Wobbly occasions. PhBodrova

With 4 banks down within the US and Europe and a minimum of a number of extra wobbling, we’re presently within the throes of the worst banking strife since 2007-08. Aggressive rate of interest hikes have meant that banks are sitting on hefty losses on their portfolios of presidency bonds – some US$2 trillion (£1.6 trillion) or 15% losses on US banks alone.

This makes many banks weak to the identical sort of funding issues that introduced down Silicon Valley Bank – one in ten banks are sitting on even better losses and tighter funding, placing the mislead any concept that SVB was uncommon. There might be potential for additional financial institution runs as anxious prospects withdraw their cash: US banks alone have over US$1 trillion in uninsured buyer deposits. All eyes will probably be on Deutsche Bank and First Republic to see if they’ll overcome the market jitters of the previous few days.

The Federal Reserve and different central banks are reassuring everybody that the monetary system is sound and bears little comparability to 2008. Nonetheless, there are a selection of foreseeable penalties for the medium time period which are barely being mentioned but.

1. Weaker financial institution lending

When somebody borrows cash, they usually must pay additional to borrow for an extended period than a shorter period, as a result of it’s typically riskier to lend additional into the long run. But this flips when buyers get nervous concerning the fast future, which is what has occurred proper now (we are saying the yield curve has inverted). This factors to a recession within the coming months.

Banks are already reluctant to lend as a result of they’re having to pay extra to borrow from each other at right now’s rates of interest. Therefore the broader financial uncertainty is more likely to make it even tougher for customers and companies to get credit score. In the aftermath of the 2007-09 disaster, US financial institution lending fell by nearly 11% .

2. Government borrowing difficulties

Banks have gotten into bother from investing in long-term authorities bonds, supposedly one of many most secure belongings available in the market, which raises questions on to what extent they are going to be keen to take action in future. Governments sometimes situation bonds of upwards of a yr to finance long term or larger-scale investments, however could discover this tougher at a time when there are hefty payments to pay.

For occasion the ageing of the large child boomer era is placing important stress on healthcare, requiring heavy authorities funding into medical analysis, healthcare infrastructure and additional employees. The inexperienced industrial coverage agenda entails huge prices too.

If banks should not keen to purchase long-term bonds are readily as earlier than, the price of borrowing will rise at a time when most governments are already fighting excessive ranges of debt.

3. More inflation

Central banks might step in and purchase extra authorities bonds instantly to supply their governments with the mandatory funds. Unfortunately that is tough, since such purchases would probably enhance the cash provide and make inflation worse than it’s already.

Inflation has tailed down a bit of in international locations such because the US and UK for the reason that peaks of 2022, however continues to be nicely above the two% goal. If central banks must instantly assist extra authorities borrowing, anticipate extra upward stress on costs. This in flip will put extra stress on central banks to maintain rates of interest increased.

So far, the Federal Reserve (the US central financial institution), has tried to minimise the harm by establishing a facility to permit banks to borrow towards their authorities bonds at e-book worth. In simply a few weeks, US banks have already borrowed practically half a trillion US {dollars}. But once more, there are limits to how a lot help could be supplied with out jeopardising the combat towards inflation.

4. Fewer jobs

So far, the roles market within the US and likewise the UK has been pretty resilient. But if credit score turns into extra scarce and there’s a recession, that scenario might change fairly shortly.

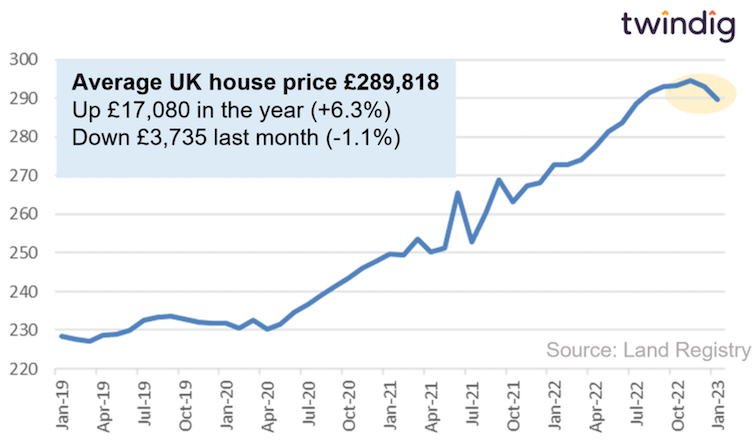

5. Lower home costs

The housing market within the US and UK has additionally held up fairly nicely, regardless of increased rates of interest. But in an atmosphere of extended excessive rates of interest and lowered financial institution lending, home costs might begin falling extra sharply: after the 2007-09 disaster, US home costs fell by nearly 20%.

UK common home costs

Twindig

6. Less client spending

With households already having to seek out extra to cowl increased mortgage funds, client spending is struggling. A fall in home costs and an increase in unemployment will additional have an effect on how rich folks suppose they’re, which might additional scale back how a lot they’re keen to spend.

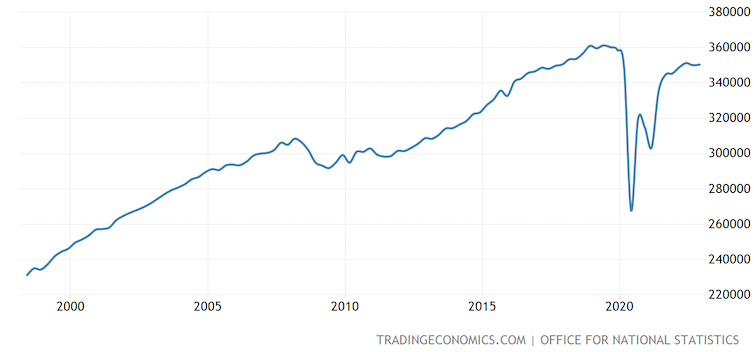

UK client spending

The y-axis present client spending in hundreds of thousands of £. Note that it doesn’t take account of inflation.

Trading Economics

7. The demise of smaller banks

To forestall financial institution runs, governments might additionally step in and probably insure all buyer deposits: within the US, for instance, prospects’ cash is just protected as much as US$250,000, whereas within the UK it’s £85,000. The drawback with extending this safety is that it could be each costly and troublesome to get previous politicians because it means rescuing rich folks.

This is why US treasury secretary, Janet Yellen, just lately stated this wasn’t an choice, besides perhaps for large banks whose collapse might pose a systemic danger – which means it might threaten your entire international banking system. Yet in the event you give better deposit safety to those banks, you make them safer than the smaller banks – certainly, they have already got harder funding necessities within the US.

The hazard is that increasingly more prospects transfer their cash to the larger banks, making it extra seemingly that the smaller banks collapse. Consumers would then have fewer banks to select from and will find yourself paying increased costs for monetary companies or have much less entry to monetary merchandise.

This all factors to robust selections forward for governments and central banks. At the very least it appears to be like seemingly that rates of interest might want to come down to assist shield banks, which can imply that we have now to dwell with increased inflation for longer than most individuals had been anticipating.

![]()

Konstantinos Lagos doesn’t work for, seek the advice of, personal shares in or obtain funding from any firm or group that may profit from this text, and has disclosed no related affiliations past their educational appointment.